Capital expenditure (capex) for the first quarter (January - March 2018) is due Thursday 31 May 2018

- At 0130GMT

I posted a preview here earlier:

More now, via:

NAB:

- As the remaining GDP partial for investment in Q1, CapEx numbers will be watched carefully, particularly following slightly softer-than-expected Construction Work Done data earlier in the week.

- NAB is expecting the data to report a modest 0.5% q/q increase in capital spending, below market consensus of 1% q/q.

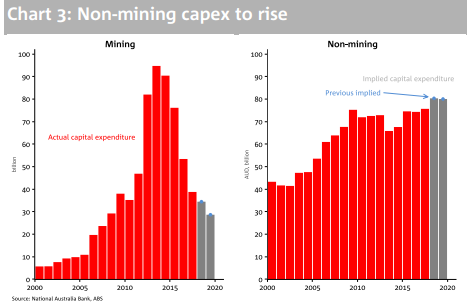

- Breaking down NAB's forecast, mining CapEx is expected to lift a little (+1.5% q/q), after last quarter's 4.7% q/q fall. There are signs that mining investment has bottomed, with increased reports of growing sustaining capex and return in greenfield exploration investment. While resource-related projects have very long lead times and will take some time to show up in mining capex, these signs - in combination with higher Q1 engineering work done - suggest the underlying trend is turning positive.

- For non-mining capex, recent quarters have reported strong growth - a welcome sign of the broadening strength in the Australian economy. Nevertheless, we expect March quarter to show that non-mining capex has taken a moment to catch its breath, growing a modest 0.4% q/q, to bring year-ended growth to 8%. Such a softening in growth would be consistent with the decline in non-residential construction noted in the Construction Work Done data.

- Like non-mining capex, non-dwelling work done has seen a few quarters of strong growth, prior to the softer Q1 print. We suspect the recent decline in Q1 non-dwelling construction is a blip, but one that will also be reflected in the capex numbers this quarter. Going forward, underlying factors - strong demand for offices and warehousing - should be supportive.

- Taken together with mining capex, this implies 0.5% overall capex growth in the quarter, and a softening of year-ended capex growth to 3.3%.

- In the CapEx data, often of equal (if not more) interest is the forward estimates for capital spending. NAB expects these estimates to shows businesses expectations for spending in 2017-18 improved moderately (Estimate 6: $117.8b), while 2018-19 expectations were broadly unchanged (Estimate 2: NAB $90.3b; Mkt $90.5b).

RBC:

- We look for a 1% rise in capex in Q1 with an increase in plant & equipment expenditure likely offset by a decline in non-residential spending based on early partials.

- On an industry basis we expect a continuation of recent trends with a further rise in non-mining capex and a small fall in mining capex with the drag from this sector almost complete.

- The expenditure plans will remain in focus with a likely modest upward revision to the current FY2017-18 and we would also anticipate an upward revision to the disappointing first cut of plans for FY2018-19 given stellar business conditions and continued buoyant business investment.