Australian second quarter CPI data is due this week, on Wednesday 23 July 2018 at 0130GMT

For the 'headline'

- expected +0.5% q/q

- prior was +0.4%

For the y/y headline rate

- expected 2.2%

- prior 1.9%

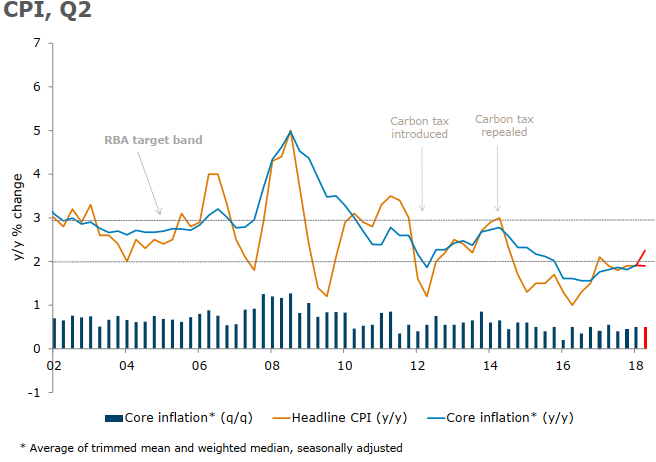

For the 'trimmed mean' (which is the measure the RBA pays most heed to - its the 'core' inflation figure where the RBA target band is 2 -3%)

- expected 0.5%

- prior 0.5% q/q

For the trimmed mean y/y result

- expected 1.9%

- prior 1.9%

Finally, there is the 'weighted median' CPI, also a core measure:

- expected 0.5% q/q

- prior was 0.5%

For weighted median y/y,

- expected 1.9%

- prior was 2.0%

Preview via ANZ:

- We expect Q2 inflation data to show that any acceleration in inflationary pressures remain very gradual. Headline inflation will likely tick up to 0.5% q/q, due to a rise in petrol prices, the seasonal increase in health insurance premiums and the regular tobacco indexation.

- Core inflation is expected to be steady at 0.5% q/q and 1.9% y/y, just below the RBA's target band. Weak wage pressures and retail competition continue to weigh on core inflation.

Via RBC:

- We expect headline CPI to have risen by 0.6% in Q2, lifting the y/y rate to 2.3% boosted by some base effect.

- The average of the key core measures (trimmed mean and weighted median) are likely to be slightly more modest at 0.5% with the y/y edging marginally lower to 1.9% from just under 2%. This would be slightly below the RBA's latest forecast. We expect other underlying measures to be more benign with the market sector ex-volatiles continuing to run not far from 1% y/y.

- With ongoing slack in the labour market and annual unit labour costs barely positive coupled with ongoing competition and disruption, we expect core inflation to remain ~2% for much of the next 12 months.