Australia Private Capital Expenditure for April to June (second quarter) is due Thursday 30 August 2018 at 0130GMT

I have posted previews earlier:

- AUD data due - preview of Q2 capex (ANZ)

- preview here via NAB

This now via Westpac, looking first at the 'headline' (consensus is 0.6%, previous was 0.4%):

- Business capex spending turned the corner in 2017, with the mining investment wind-down almost complete and an emergence upswing in non-mining investment. Capex rose 4% in 2017 after four years of decline.

- In 2018, capex edged 0.4% higher in Q1 and we anticipate a rise of 0.4% in Q2.

- Building & structures capex is expected to slip, declining by 0.3%. The Construction Work survey reported that infrastructure activity fell (as gas projects are completed), largely offset by a rise in non-residential building work.

- Equipment spending has trended higher since mid-2017, emerging from a soft spot over the second half of 2016. We anticipate a further gain in Q2, a forecast +1%. Profits are up, so too capacity utilisation levels, global growth has been strong and there are positive spill-over effects from the strong upswing in public infrastructure.

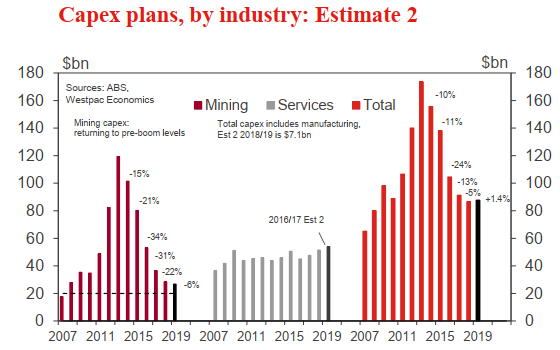

Also of most interest to the market are capex plans. WPAC again:

- This survey, conducted during July and August, includes the 3rd estimate of capex spending plans for 2018/19.

- In the previous survey, Est 2 for 2018/19 was $87.7bn, 1% above Est 2 a year ago. This is the first positive 'Est 2 on Est 2' comparison since 2012/13.

- For mining, Est 2 on Est 2 is only a modest negative, at -5.8%. For services, Est 2 vs Est 2 is +4.8%, evidence that the investment upswing is set to continue.

- This update is likely to confirm the broad themes evident in the capex survey 3 months earlier. However, as to the value of Est 3, we see the risk of some apparent slippage.

- For Est 3 on Est 3 to be at +1% (matching the Est 2 on Est 2 outcome) would require an upgrade to $104bn. That is a hefty 19% above Est 2 - yes the same upgrade as this time last year, but that was an abnormally sharp increase (the largest since 1988/89). A figure around $102bn, -1% vs Est 3 a year ago, may be more achievable

(bolding in the above is mine)