I posted two here earlier:

Due at 0130GMT

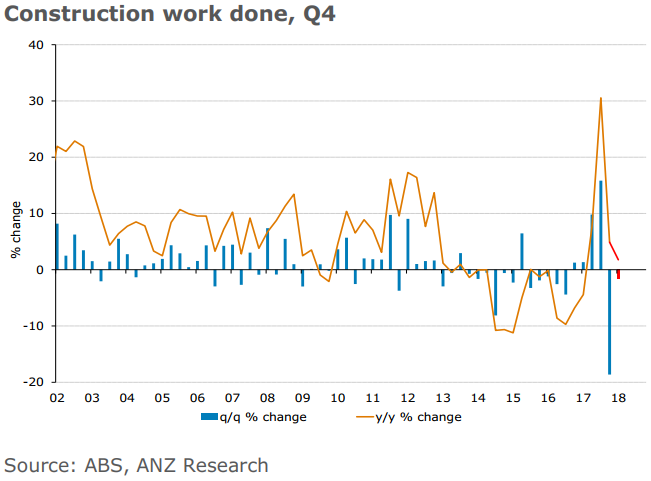

- expected +1.3% q/q

- prior -19.4% q/q

ANZ:

We believe construction fell again in Q1, as we return to normality following the LNG import-affected results over the previous three quarters.

- The main driver of the quarterly weakness is expected to be in the engineering sector, as the final dregs of the mining investment boom are completed.

- On the other hand, a record backlog of work in the housing sector is likely to see residential construction nudge higher over the near term.

NAB:

Construction Work Done is expected to report Q1 activity lifted modestly, the consensus looking for growth of 1.3%. NAB's expectation is similar, a 1.5% rise in the March quarter, following the past two quarters of volatility that were affected by a major facility component for the massive Inpex Ichthys LNG project that is getting closer to full start up.

- Building work done is expected to increase 0.6% q/q, as non-residential construction continues to lift (+2.7% q/q), alongside reports of a tight commercial property market, particularly in offices, warehousing and accommodation. The growth in non-residential building is expected to offset the gradual slowdown in residential building (-0.6% q/q), as the housing construction cycle and the market continues to emit signs of cooling.

- Engineering work done could be the swing factor, again, and it is expected to increase 2.7% q/q. This component of Work Done has been lumpy as the import of large LNG components resulted in a sharp rise and fall in Q3 and Q4 payback last year. This quarter, we expect Engineering work done to rise as mining services and maintenance picks up alongside higher commodity prices, while road and transport infrastructure construction should be more evident with much more growth to come.

Trade REAL stocks and cryptos on a single platform!