Fed President speaking to thousand 25 US monetary policy forum

U.S. central bank does not need to be in a hurry to adjust interest rates

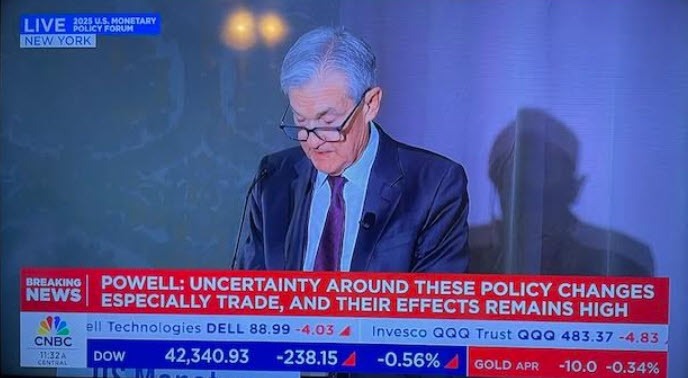

Uncertainty around Trump administration policies and their economic effects remains high

Some near-term survey and market measures of inflation expectations have moved up driven by tariffs

Most longer-term inflation expectations remain stable, consistent with 2% goal

Fed is well-positioned to wait for greater clarity

Net effect of trade, immigration, fiscal, and regulation policy is what matters for economy, monetary policy

Fed policy not on preset course; can maintain policy restraint for longer if inflation progress stalls, or ease if labor market unexpectedly weakens or inflation falls more than expected

U.S. economy in a good place, despite elevated uncertainty

Labor market solid, broadly in balance; inflation somewhat above 2% goal but moving closer to target

Path to 2% inflation will be bumpy; Fed does not overreact to one or two readings that are higher or lower than anticipated

Labor market not a significant source of inflationary pressure

Recent indicators point to possible moderation in consumer spending, heightened uncertainty; remains to be seen how these developments may affect future spending, investment

Repeats that 2% inflation goal is not a focus of Fed's framework review; results due late summer