It is vital to be careful about over-responding to high-frequency data, which contrasts with the perspective of financial markets

I am of the opinion that inflation expectations have not lost their anchor

The outlook for inflation seems less bleak than in 2022, largely due to increased slack in the labor market

Maintaining focus on the core goal of hitting the 2% inflation target is essential

Trade-offs must be considered, yet the priority of the inflation mandate should be highlighted

Monetary policy cannot resolve issues stemming from real economic shocks; a genuine structural adjustment will be required

Reaching the inflation goal is somewhat in jeopardy; we must prioritize policies that offer the best protection against a 2022 recurrence

The current path is clear when compared to where things stood six weeks ago

My perspective on "wait-and-see" approaches is that you must define exactly what data you are looking for

I am not convinced that simply waiting is the most effective reaction

It remains an open question whether maintaining current rates is a sufficiently restrictive form of tightening

I would prefer that my MPC colleagues do more than just state we are taking a "wait-and-see" stance

Bank of England Chief Economist Huw Pill signaled a growing impatience with passive monetary policy, challenging the "wait-and-see" mantra adopted by some of his colleagues and calling them out directly. Pill argued that simply holding rates may not be a sufficient form of tightening, especially as the path toward the 2% inflation target remains "at risk." While he acknowledged that the labor market currently shows more slack than during the 2022 crisis—helping to keep inflation expectations anchored—he warned that monetary policy is not a cure-all for "real" economic shocks, which require deeper structural adjustments.

Pill’s rhetoric suggests a desire for more proactive insurance against a repeat of past inflationary surges. He cautioned against overreacting to volatile, high-frequency data favored by markets, advocating instead for a disciplined focus on the primary inflation mandate. By pushing the MPC to define clear triggers for action rather than just observing, Pill is positioning himself as a leading voice for a more assertive, "policy-as-insurance" approach to ensure price stability is not just maintained, but secured.

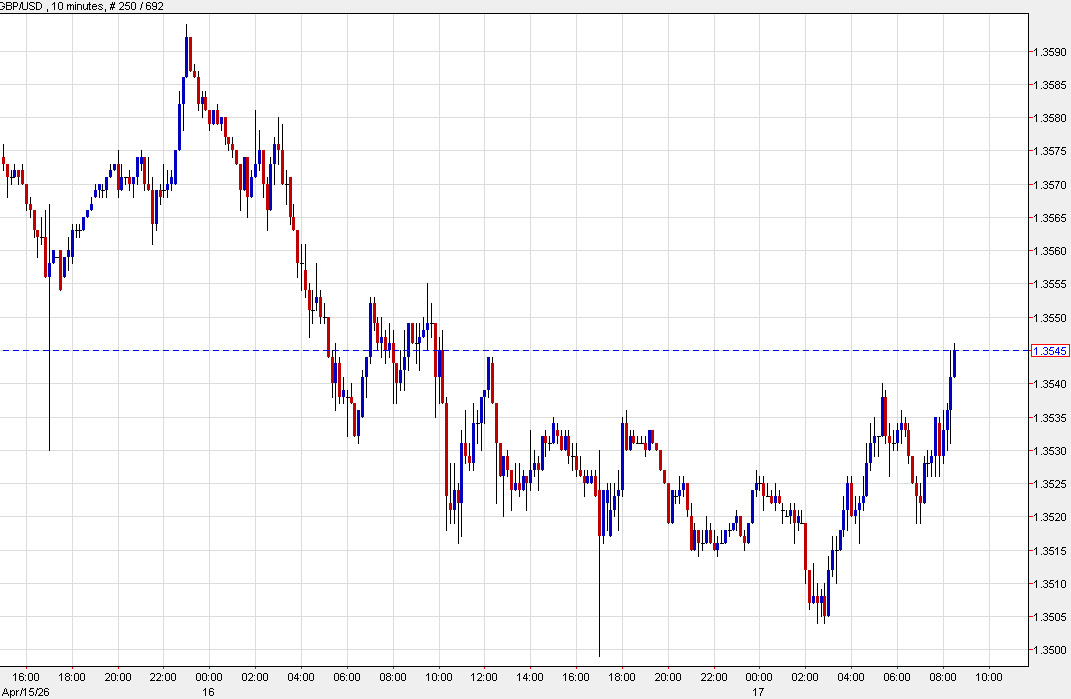

In light of the comments (and broad positive risk sentiment), the pound is at the highs of the day, up 22 pips to 1.3545. The market is pricing in a 43% chance of a hike at the June meeting.