Two currencies that shaped global markets for the past 70 years are losing their status. The yen is no longer the world’s free credit line and the dollar is no longer the clean safe haven. That vacuum has to be filled by somebody — and everything now points to the Swiss franc — both the world’s new funding currency and its ultimate refuge.

The yen under pressure

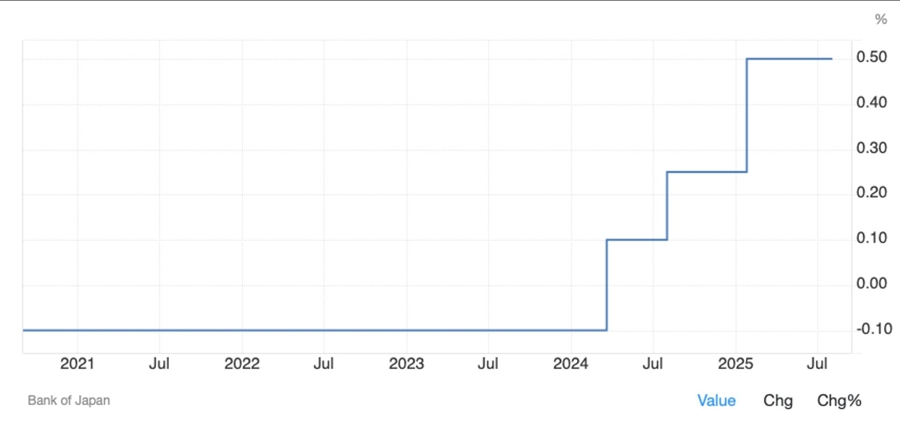

For thirty years the yen symbolized cheap money and powered global carry trades. But today, that reality has burned out. The Bank of Japan drowned in policy chaos, inflation is stuck, and the USDJPY exchange rate has broken through 160. What was once seen as the ultimate safe haven has become a liability. The market is already moving on.

Carry trade was born in Tokyo. From the late 1990s to December 2024, investors borrowed yen at zero and poured it into everything with yield. But from January 2022 the whole structure started to collapse: the yen crashed to 150 per dollar, credibility evaporated and volatility exploded.

In January 2025, the BOJ finally moved — hiking to 0.5%, the highest level in 17 years. Why? Because inflation was no longer an illusion.

Tokyo CPI pushed past 2.5%, food and energy costs surged, and domestic demand finally showed up. Add in the pain of higher import costs from a weak yen, and zero rates were no longer an option. And now economists expect another step to 0.75% before year-end.

The dollar’s problem

The dollar used to jump whenever markets got scared. Not anymore. Washington keeps using it as a political weapon — tariffs on rivals, sanctions on Russia, trade fights with India and anyone else who refuses to play by its rules. The logic was clear: force the world to use dollars and demand would stay locked in.

But politics cuts both ways. Instead of tightening their grip, sanctions and tariffs pushed countries to experiment with alternatives — oil deals settled in yuan, sovereigns raising debt in francs, central banks trimming their dollar share.

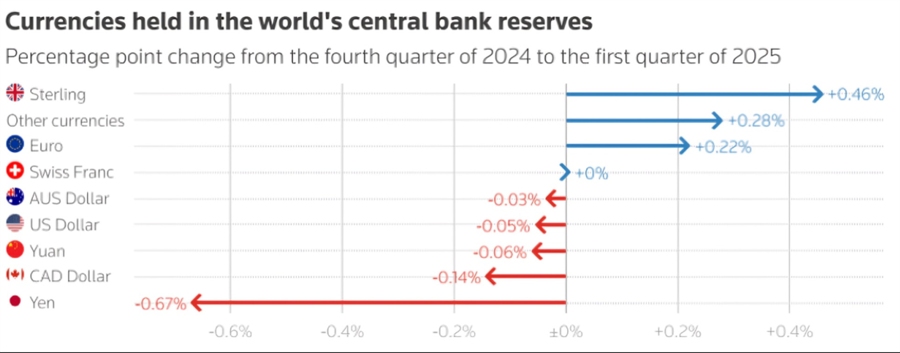

IMF’s COFER data for Q1 2025 shows the dollar’s share of global reserves edging down to 57.74%, while the pound slipped to 4.7%. The Swiss franc, though small, is finally moving the other way — its share has inched higher for the first time in over a decade. For reserve managers, that shift is symbolic: the franc is no longer a niche, it’s becoming a credible alternative.

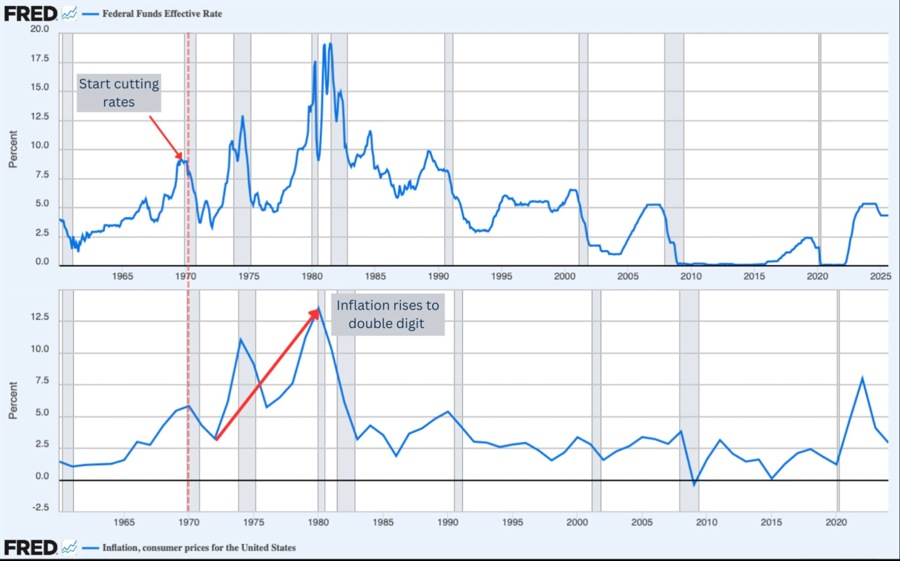

The data tells the same story. The revisions wiped out 911,000 jobs — nearly a million paychecks that simply vanished. August payrolls added just 22,000 instead of the 75,000 expected. That’s not a slowdown — that’s a halt. Unemployment is stuck at 4.3%. And inflation? It’s not easing. CPI jumped 2.9% year-on-year, while core held at 3.1%. That’s not cooling — that’s re-accelerating.

And here’s the danger. Markets still expect the Fed to cut rates this week — even as inflation ticks higher. Apollo, a Wall Street giant, warns the setup looks eerily like the 1970s: inflation dipped, then came roaring back in two brutal waves. If the Fed eases now, it risks the same trap — weaker growth, hotter prices, and an even deeper loss of trust in the dollar.

History also shows another danger: market crashes often start not at peak rates, but right after cuts begin. When the Fed blinks, it usually means the economy is already cracking — and that’s when confidence truly unravels.

The vacuum and the rise of the franc

While the yen collapsed as funding and the dollar lost its haven shine, the market searched for a replacement. The euro is stuck in recession. The old anchors are gone. That left a vacuum — and the franc stepped straight in.

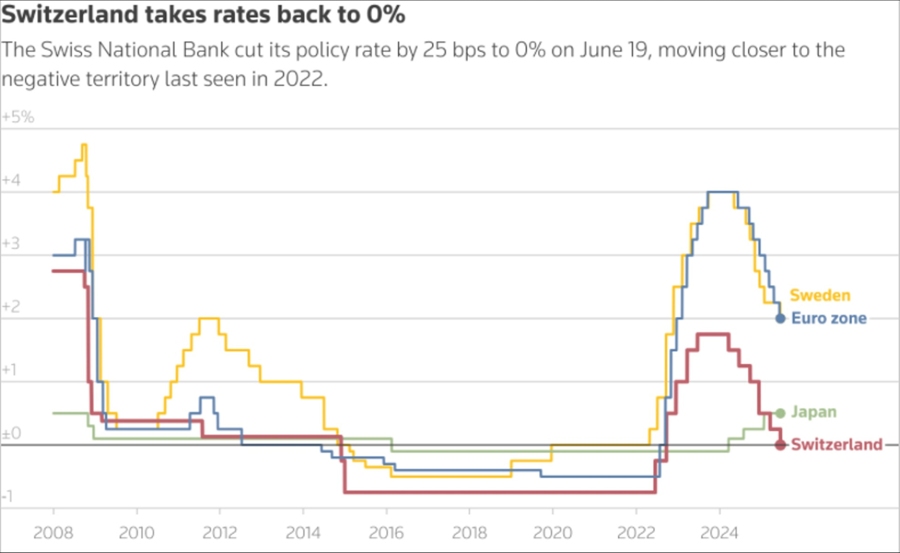

In 2025, CHF surged 11% against the dollar, while EURCHF slid to historic lows. Normally a rally like this would scare off investors. Instead, demand accelerated right after the SNB cut rates to 0% in June.

The reason? The central bank sent the opposite message: no return to negative rates, no heavy-handed interventions, no more defending “floors” in EURCHF. SNB Chairman Martin Schlegel even spelled it out: “The barriers to reintroducing negative interest rates are very high.”

Meanwhile, Swiss inflation has disappeared. In May, CPI printed –0.1% y/y — first deflation since COVID. For exporters, a stronger franc is painful. For global capital, it’s a green light: stability, no inflation risk, and a central bank willing to let the currency run. That combination makes the franc unique — 0% for funding, and a safe haven when the world cracks.

In short, the franc is what the yen once was — without the chaos, without the policy circus, with far more credibility. And it’s not just theory. Capital flows already prove it — sovereigns, funds, and banks are treating the franc as the new anchor.

The world is already moving

It’s not just Zurich policy or Swiss inflation anymore — the rest of the world is proving the shift with money on the table. This year, Panama secured nearly $2.4 billion in Swiss franc loans from banks this year, saving more than $200 million compared with dollar borrowing. Colombia, Sri Lanka and Kenya — they’re all running the same math: why pay a premium for USD when the franc is cheaper and cleaner?

The crisis tape tells the same story. When Israel struck Iran in June, the USDCHF rate initially rose — a reflex reaction to the dollar. But this movement did not last long. Within a few days, the market reversed, and the franc rose to new multi-year highs. Nobody was running to Treasuries. The yen didn’t even show up. The bid went straight into francs, fast and heavy.

Even banks are joining the move. Sight deposits at the SNB spiked CHF 11.2 billion in July, pushing reserves to their highest in over a year. Institutions aren’t waiting for theory — they’re already parking liquidity in francs, getting ready for the next shock. Emerging market borrowers are increasingly turning to Swiss francs in their financing mix. Several EM issuers chose CHF in recent deals. The IFC, for one, issued a CHF 155 million social bond — its largest to date in this currency.

Put it all together and the verdict is brutal: the yen has burned out, the dollar is bleeding trust, and capital has already chosen its new home. The franc isn’t waiting for the future — it’s already the safe haven of the present.

Market reaction

The shift is already visible on the screens. USDCHF has turned into the new fear gauge: when markets shake, the dollar falls and the franc rips higher. USDCHF has broken down from its consolidation triangle, pointing straight toward fresh lows. The first target sits near 0.787, with the 13-year low not far behind. And with RSI still mid-range, below 50 but far from oversold, the message is simple: CHF strength isn’t spent. It’s only beginning.

FX desks that once defaulted to JPY for carry are now building structures around CHF. Even with rates at 0%, demand for Swiss francs hasn’t dried up — rather, it has accelerated.

Conclusion

Two pillars of the postwar FX world are crumbling. The yen can’t fund, the dollar can’t shelter. The market doesn’t wait for nostalgia — it needs a currency that works now. And the flows already show where it’s going.

The Swiss franc has become the only hybrid left: 0% money for funding, hard-as-stone credibility for refuge. Zurich offers what Tokyo lost and what Washington squandered.

The yen’s era is over. The dollar’s safe-haven myth is breaking. For the first time in 70 years, the world has a new anchor — and it’s Swiss.